A sparkling swimming pool represents the ultimate backyard dream for countless homeowners, but substantial upfront investment often creates barriers. Strategic financing opens doors to immediate pool ownership while preserving cash reserves.

Mission Pools brings over three decades of experience helping homeowners navigate both construction and financing decisions, providing transparent cost estimates and guidance for informed financing choices.

Most homeowners finance their pool projects rather than depleting savings accounts. And for good reason.

Pool financing helps you spread costs across manageable monthly payments while preserving cash reserves for emergencies, investments, or other home improvements that pop up.

Financing enables immediate enjoyment of your investment rather than waiting years to accumulate cash. This is especially valuable if you’re a family with young children, as pools provide maximum family benefit during prime childhood years that can’t be recaptured later.

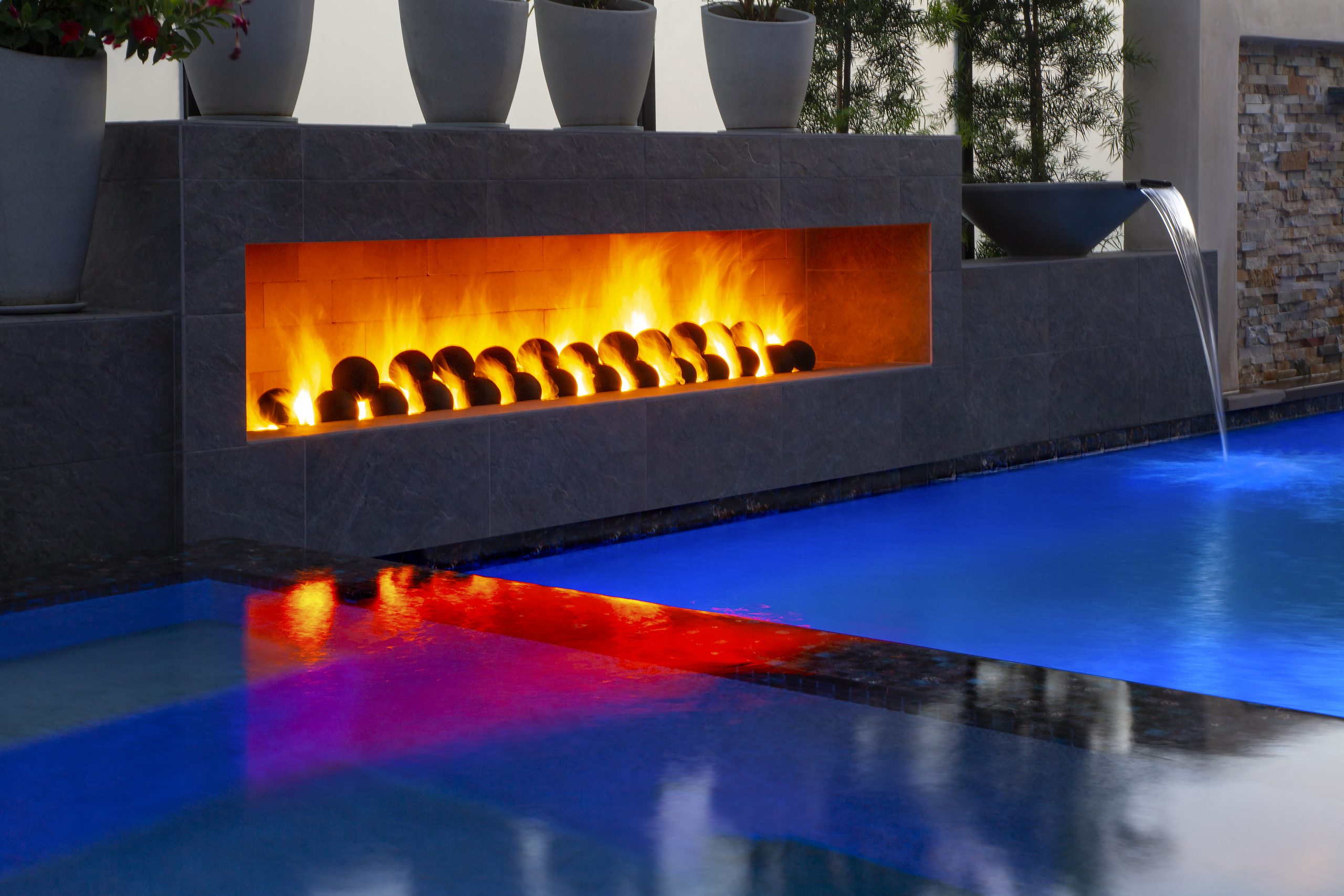

Strategic financing also unlocks upgrade opportunities that might otherwise remain financially out of reach to you. The difference between basic and premium features often represents a relatively small increase in monthly payments while delivering significant long-term value and enjoyment.

However, financing does carry inherent risks including:

You should also keep in mind that pools rarely provide dollar-for-dollar returns in home valuations, making financing decisions primarily lifestyle-driven rather than investment-focused.

Pool financing proves especially beneficial for larger projects exceeding $50,000, luxury installations with extensive features, or commercial properties where pools generate revenue streams that offset financing costs.

Accurate cost estimation forms the foundation of smart financing decisions, as underestimating project scope leads to funding shortfalls and financial stress during construction.

Comprehensive pool projects involve multiple cost categories beyond basic construction, including site preparation, permits, utility connections, landscaping, and ongoing operational expenses.

Professional estimates should encompass excavation and site work, structural components and plumbing, equipment installation and electrical connections, decking and surrounding hardscaping, plus landscaping integration and cleanup. Additional considerations include permit fees, inspection costs, utility upgrades, and water filling expenses.

Smart planning includes 10-20% contingency allowances for unexpected site conditions like poor soil, underground utilities, or drainage issues that surface during excavation. Change orders during construction, upgrades to materials, additional features, or design modifications will add costs that exceed initial budgets.

We at Mission Pools provide detailed, itemized estimates that break projects into clear phases, helping clients understand cost components and plan financing accordingly. Comparing multiple contractor estimates reveals market pricing while highlighting potential cost variations based on materials, features, and construction approaches.

You should also consider lifecycle costs including ongoing maintenance, utility expenses, and eventual equipment replacement when evaluating total ownership costs. These operational expenses don’t require immediate financing but impact long-term budgeting and overall project affordability.

Home equity loans and HELOCs leverage your property’s value to secure favorable financing terms. Traditional home equity loans provide lump-sum funding with fixed rates, while HELOCs offer flexible credit lines with variable rates. The primary advantage is typically lower interest rates compared to unsecured financing, often 2-4 percentage points below personal loan rates.

However, your home becomes collateral, creating foreclosure risks if payments become difficult. These products require sufficient property equity, strong credit scores, and detailed income verification. Most lenders limit combined mortgage and equity debt to 80-85% of property value, so borrow only what you can comfortably repay.

Personal loans provide streamlined financing without collateral requirements, making them attractive for homeowners with limited equity. Online lenders, banks, and credit unions offer competitive products with quick approvals and fast funding timelines. Benefits include simplified applications, faster approvals (often within days), and no lien against your property.

Drawbacks include higher interest rates reflecting increased lender risk and shorter repayment terms typically ranging 3-7 years. Personal loans work especially well for smaller projects under $75,000 or homeowners who value speed over lowest rates. Rate shopping proves essential, as rates vary significantly between lenders.

Specialty construction loans offer disbursement schedules aligned with project phases, releasing funds as work progresses rather than providing upfront lump sums. Pool-specific lenders understand construction processes and offer products tailored to swimming pool projects. These loans often convert to traditional term loans upon completion, providing predictable long-term payment structures.

Advantages include professional oversight of fund disbursement and protection against contractor payment issues. Potential drawbacks include more complex documentation requirements, mandatory inspections at each funding phase, and potentially higher rates compared to home equity products. Fund availability depends on construction progress, requiring careful coordination with contractor schedules.

Cash-out refinancing replaces your existing mortgage with a larger loan, providing the difference in cash for your pool project. This approach works best when current rates equal or exceed your existing rate, or when consolidating other high-interest debt. Primary benefits include accessing substantial funds at mortgage rates and extending repayment terms to minimize monthly payment increases.

Considerations include closing costs typically ranging 2-5% of loan amounts and extended repayment terms that increase total interest costs. Rising interest rate environments make cash-out refinancing less attractive compared to preserving existing low-rate mortgages. This strategy proves most effective for large projects exceeding $100,000 or when debt consolidation opportunities provide additional benefits.

Many pool contractors offer financing partnerships with specialized lenders or direct payment plans that simplify the financing process. Benefits include one-stop shopping for both construction and financing, potentially competitive promotional rates, and simplified coordination between funding and construction phases. Some contractors offer seasonal promotions with reduced rates or extended payment terms.

However, contractor financing may carry higher costs than independent shopping and limited lender competition. Always verify actual interest rates, fees, and terms before committing to contractor-arranged financing. Evaluate contractor financing alongside independent options and request detailed financing disclosures to compare total costs including any hidden fees or rate adjustments.

Credit cards serve limited roles in pool financing, primarily for small project components or short-term funding bridges. Responsible usage involves leveraging 0% introductory APR periods for specific purchases while maintaining ability to pay balances quickly. Advantages include immediate fund access, potential rewards benefits, and flexibility for smaller purchases like permits or materials.

Major drawbacks include extremely high interest rates (often 18-25% APR) if balances carry beyond promotional periods. Credit limits are typically limited relative to pool project costs, and high balances can negatively impact credit scores. Strategic usage involves paying promotional balances before rate increases and using cards only for amounts you can repay quickly.

Various government programs, utility companies, and municipal authorities offer incentives for energy-efficient pool equipment, solar installations, or accessibility improvements. Benefits include direct cost reductions through rebates or grants, preferential loan terms for qualifying improvements, and long-term operational savings. Some programs offer significant rebates for solar heating, efficient pumps, or LED lighting installations.

Limitations include qualifying criteria restrictions, limited funding availability, and application complexity. Program availability varies significantly by location and changes annually based on funding allocations. Research local utility rebates, state energy programs, and municipal incentives early in planning processes through resources like the Database of State Incentives for Renewables & Efficiency.

Effective financing comparison requires evaluating multiple factors beyond basic interest rates, including total costs, payment structures, risks, and flexibility. Create comparison frameworks that consider annual percentage rates (APR), monthly payment amounts, total interest costs over loan terms, and associated fees.

Key evaluation criteria include:

Use amortization calculators to compare scenarios across different rates and terms. For example, a $75,000 pool financed at 6% over 10 years requires $832 monthly payments totaling $99,840, while the same amount at 4% over 15 years requires $555 monthly payments totaling $99,900.

Include budget buffers ensuring monthly payments remain comfortable during income fluctuations or unexpected expenses. Financial advisors typically recommend total debt payments remain below 36% of gross monthly income, including mortgage, pool loan, and other obligations.

Consider rate type stability, choosing fixed rates during rising rate environments and variable rates when expecting declining rates. Evaluate prepayment flexibility for paying loans early without penalties, especially important for homeowners expecting windfalls or income increases.

Strategic cost management reduces both initial financing expenses and long-term borrowing costs through careful planning and smart financial decisions.

Post-approval processes vary significantly between financing types, with construction loans requiring the most oversight and traditional loans providing immediate full funding. Many lenders require inspection verification before releasing funds, ensuring work completion meets standards before payment. Coordinate disbursement timing with contractor payment schedules to avoid cash flow issues.

Document and approve any changes to original project scope, ensuring adequate funding for modifications that may require loan adjustments. Maintain communication with both contractors and lenders throughout construction phases to address issues promptly. Complete final inspections, obtain lien waivers from all contractors and suppliers, and verify permit closure before final funding disbursement. Proper documentation protects against future legal issues and ensures warranty coverage.

Pool renovations typically require smaller financing amounts and simpler approval processes compared to new construction projects. Renovation scope varies dramatically from basic resurfacing ($10,000-25,000) to comprehensive rebuilds approaching new construction costs.

Multiple financing pathways make dream pools accessible across diverse budgets. Success requires careful cost estimation, thorough rate shopping, and realistic budget planning.

Contact Mission Pools today for comprehensive project estimates and financing guidance that helps transform your backyard dreams into reality through transparent cost breakdowns and trusted financing partner connections.

Most lenders require minimum credit scores of 600-650 for pool financing, though the best rates typically require scores above 720. Home equity products may have slightly lower requirements due to collateral security, while personal loans often require higher scores. Improving your credit score by even 50-100 points can significantly reduce interest rates and save thousands over loan terms.

Borrowing limits depend on financing type and individual qualifications. Home equity loans typically allow borrowing up to 80-85% of home value minus existing mortgage balance. Personal loans often cap at $100,000-150,000 for qualified borrowers. Construction loans may provide higher limits based on project scope and property value.

Always compare contractor financing against independent options. While contractor financing offers convenience and sometimes promotional rates, independent shopping often provides better terms and more options. Request detailed financing disclosures from contractors and compare total costs including all fees and rate adjustments before deciding.

Yes, but debt-to-income ratios significantly impact approval and rates. Most lenders prefer total monthly debt payments below 36-43% of gross income, including the new pool loan. Pay down existing debt before applying, or consider debt consolidation through cash-out refinancing if beneficial.

Cost overruns require additional funding through personal savings, credit cards, or supplemental loans. This highlights the importance of accurate initial estimates and contingency planning. Some construction loans allow modification for approved change orders, but additional funding often requires separate approval processes.

You know . . . you just do not wake up one day and decide you can be someone’s partner in business. Strong relationships take...

Southern California is known for a lifestyle second to none. Our area that started out as an arid desert has now become a land of...

Yesterday was an example of why my brother and I enjoy this business so much. Contracting is all about solving problems…problem/solution management.